What Do Fed Rate Cuts Mean For Mortgage Rates?

When you hear on the news that “the Fed is cutting rates,” it’s easy to assume mortgage rates will automatically drop too.

But that’s not how it works.

Let’s break this down in simple terms.

What the Fed Actually Controls

The Federal Reserve sets something called the Federal Funds Rate (FFR).

This is the rate banks charge each other for overnight lending, and it directly affects:

Credit cards

Home equity lines of credit (HELOCs)

Auto loans

Savings accounts

CDs

The Prime Rate (what banks charge their best customers)

So when the Fed cuts rates, these short-term consumer rates generally go down quickly.

But mortgage rates are not part of this group.

So… Why Don’t Mortgage Rates Just Follow the Fed?

Because fixed mortgage rates are based on a completely different market.

Long-term mortgage rates are driven primarily by the buying and selling of Mortgage-Backed Securities (MBS)—a type of investment similar to bonds.

Investors buy MBS the same way they buy stocks or Treasury bonds.

Their decision on where to put money depends on where they believe they’ll get the best return based on:

Inflation trends

Employment data (Jobs Reports)

Consumer Price Index

GDP

Global events (wars, oil prices, supply chain issues, etc.)

Recession fears

Stock market movement

Mortgage rates rise or fall based on how investors react to all this information, not directly on the Fed’s rate cut.

How Fed Cuts Indirectly Influence Mortgage Rates

Fed policy affects the overall economy, and that can shape investor behavior.

For example:

When the Fed cuts rates, it’s usually trying to stimulate the economy.

If investors believe inflation will cool or the economy will slow, they may move money into safer investments like bonds and MBS.

When demand for MBS rises, mortgage rates tend to improve.

But this doesn’t happen instantly.

And sometimes the markets expect a Fed cut long before it happens—meaning mortgage rates may have already adjusted in advance.

Example:

If the Fed is expected to cut by 0.25%, mortgage markets often “price that in” weeks ahead of time.

If the Fed surprises markets (either more or less than expected), mortgage rates can move suddenly—sometimes in the opposite direction.

The Big Misconception

A Fed rate cut is NOT a mortgage rate cut.

A Fed cut affects short-term consumer rates.

Mortgage rates depend on long-term market expectations, inflation outlook, and global financial trends.

Sometimes mortgage rates drop after a Fed cut.

Sometimes they rise.

Sometimes they don’t move at all.

What Does This Mean for Homebuyers Today?

Even with Fed cuts happening:

Mortgage rates will respond mainly to inflation data, economic reports, and investor confidence.

Markets have been extremely sensitive—good news or bad news can move rates quickly.

Many experts believe mortgage rates could gradually improve as inflation cools… but there is no guaranteed timeline.

Anyone trying to time the market should understand:

Mortgage rates don’t wait for the Fed—they move based on expectations, not headlines.

Bottom Line

Fed cuts are good news for many types of borrowing…

But homebuyers shouldn’t assume a Fed cut means cheaper mortgages tomorrow morning.

* See outline below for explanation.

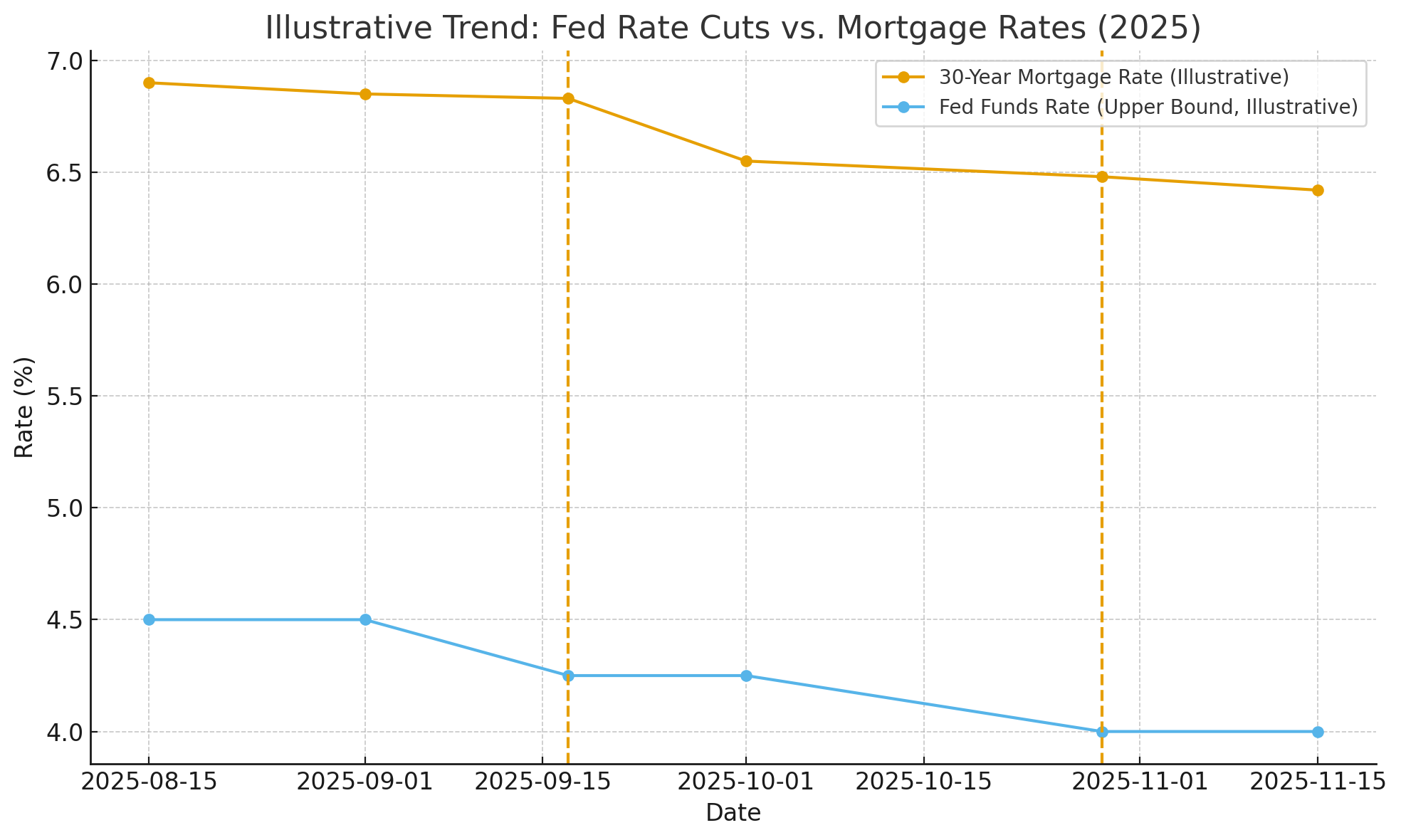

A Real-World Example — Recent Fed Cuts (2025)

The dynamics above remain very alive today — the recent cuts by the Fed illustrate just how unpredictable mortgage-rate reactions can be:

On September 17, 2025, the Fed cut its benchmark rate by 25 basis points. CME Group+2CBS News+2

Then on October 29, 2025, the Fed cut again — another 25 basis points, bringing the target federal-funds rate down to 3.75%–4.00%. Fidelity+2Trading Economics+2

But what happened to mortgage rates? The story wasn’t a clean “drop.” According to lender data:

The average 30-year fixed mortgage rate hovered around 6.8% – 7.1% for much of the first half of 2025. Bankrate+1

After the September cut, mortgage rates did eventually drift lower — by late October they were closer to 6.25% – 6.30%. Bankrate+2Bankrate+2

But that dip didn’t happen immediately after the Fed’s announcement; the movement came over weeks — not on the next day. In other words: mortgage rates lagged the Fed moves.

This shows that even when the Fed cuts rates twice in a row, that doesn’t guarantee mortgage rates will drop immediately or consistently.

What This Recent History Shows

Mortgage rates in 2025 did not fall overnight just because the Fed cut its benchmark rate.

Instead, mortgage-rate movement was gradual — influenced more by market expectations, bond yields, and investor demand than by the Fed’s statement alone.

That reinforces the idea: Fed cuts ≠ automatic mortgage-rate cuts.